Podcast: Play in new window | Download

For those of you who are new to my blog, my name is Sara. I am a CFA® charterholder and financial advisor marketing consultant. I have a newsletter in which I talk about financial advisor lead generation topics which is best described as “fun and irreverent.” So please subscribe!

What is an hourly financial advisor?

Let’s start with the basics.

An hourly financial advisor is someone who provides financial advisor for a set hourly rate. These services often include recommendations on investments, financial planning, retirement, Social Security, Medicare, tax planning, and other wealth-related topics.

Hourly financial advisors are not common. Below there is a list of advisors who charge for advice by the hour.

Checkpoint Financial Planning LLC

Family First Financial Planning

Firm Footing Financial Planning

Generational Wealth Development

Holly Donaldson Financial Planning

Kite & Compass Financial Planning

Maura Madden Financial Planning

Model Wealth- currently has a waitlist

Stewardship Financial Planning

Woodmont Financial Partners LLC

Did I leave anyone off the list? Let me know. I also want to be clear that I am not recommending any of these advisors. Please conduct your own diligence on any wealth manager you are considering hiring.

As you may have noticed, the list above is quite short. And that’s why I’m writing this blog; because I feel that financial advice rendered by the hour is a great thing for the American public (for the reasons we’re going to discuss below).

But the idea of becoming an hourly financial planner is met with such resistance you would think you told people to saw off their left arm.

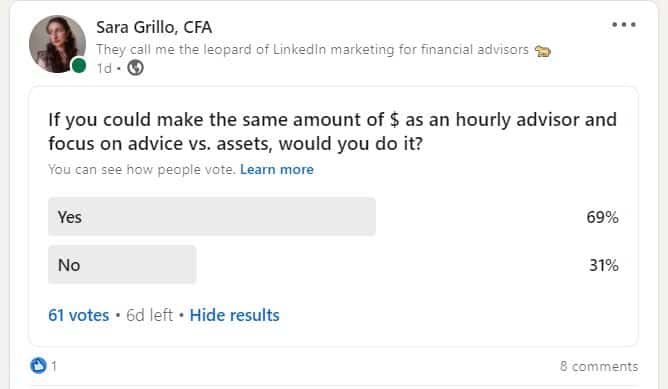

Check out this LinkedIn survey on hourly financial planners I did a while ago:

It’s pretty clear the big question in people’s minds is: can I become an hourly financial advisor and still make money? Well, here’s my interview with someone who does!

A successful hourly financial advisor: case study on Rick Ferri, CFA

Rick Ferri, CFA, decided to set up his practice as an hourly financial advisor after successfully having built a practice using other fee models. He started out at Kidder Peabody as a broker, transitioned to an RIA firm charging a 0.25% AUM fee (which is below the industry norm), which he eventually sold to start his current practice in which he charged hourly fees and renders investment and financial planning advice to clients.

Rick says that often financial advisors make things more difficult than they need to be for the purpose of job security (for example, running a Monte Carlo Simulation, sending them a 100 question long questionnaire, etc.) Ever since the beginning, Rick felt that overcharging clients for products wasn’t right. He is a follower of the late John Bogle and when he started his RIA firm he used low cost funds.

He does not take custody of assets or have discretion. His service focuses solely on advice. He conducts a two hour session with clients which is intentioned to be a portfolio check up, if you will. After the session, he provides them with a 3-5 page letter containing recommendations which they then implement on their own or hire an investment manager to execute. If they have follow up questions, he will answer over email. If they need advice a few years after the initial meeting, he can meet with them for an hour or so.

Saving investors from the “Humpty Dumpty portfolio”

Rick has delivered a high value service to investors by decluttering the “Humpty Dumpty portfolios” made by other advisors creating “complexity for the sake of job security.” As an hourly financial advisor he doesn’t make commissions for recommending products such as private REITs, structured products, etc. Because he doesn’t charge AUM fees, he’s not biased towards encouraging the clients to hire him to manage their portfolio; he often simplified the portfolio so that they can bypass having an advisor altogether and manage it themselves.

One of my favorite lines from the podcast (link at top of the page) sums it up:

“They come to me, either they have been self-managing their portfolio their whole life, or maybe they were working with…maybe a money management company…and they have come to the light. They have realized that they’re paying way too much and it’s all about smoke and mirrors in many ways, you know, complexity for the sake of job security…they’ve had their epiphany.

And when they come from another advisor and it’s this complexity-for-the-sake-of-job-security portfolio, this Humpty Dumpty portfolio that the advisor put together, it’s a restructuring. I have to kind of restructure things and make them simpler so that they can manage it.

If they’ve just converted and they have this really really messy portfolio, and they always come that way, it’s just an absolute mess of stuff, and you’ve gotta take that and you gotta bring it down to something that they can manage.”

-Rick Ferri, CFA

Why would someone decide to become an hourly financial advisor?

Rick chose to set up his practice this way because he was tired of having to be involved with products and instead wished to focus on the advice aspect of serving clients.

His clients’ net worth range from negative $300k to $100MM. The beauty of his practice is that he can help people with low assets and it makes no difference to him financially. He also has considerably less of a compliance, operational, and administrative burden because he is not taking custody or discretion of his clients’ assets. He is also agnostic as to where the clients’ assets are held. He can advise on assets held at any custodian.

This affords him the ability to work with people who are not yet wealthy but are likely to be: business owners who haven’t sold their businesses yet, doctors who are in residency burdened with debt, entrepreneurs who haven’t gone public yet, etc. He is able to fortify a bond with them before they come “into the money” so to speak which is usually when financial advisors take an interest in them – but by that point it’s too late because you rejected them when they needed you!

Rick charges $450/hour and says that he usually has one new client meeting a day and a few hours of maintenance work for existing clients. This translates into a suitable level of income for him yearly. It offers him the flexibility of not having his schedule be tied to the market.

What are the drawbacks of charging an hourly fee for financial advice?

Often financial advisors are scared to adopt the hourly fee model for the following reasons:

-

- You have to bill people at a time when they are under the most stress (divorce, selling a business, etc.)

-

- People are reluctant to call for fear of running up the tab

-

- Hard/annoying to track

-

- Hard to get people to come back

-

- It feels transactional

-

- Hard to scale

…to which I would argue:

Having to charge people at stressful times – you’d be charging them if you worked on AUM fees or a flat fee as well. Wouldn’t ya? If you aren’t comfortable enough with your value proposition to send someone a bill, it’s time to revisit your value proposition.

Running up the tab – How you manage the client matters. If you do a good job establishing a sense of what it important in the relationship and gathering information in the beginning, this is less of a concern.

Hard to track – If you’re saying that it’s because you’re probably one of those advisors who doesn’t know how to/doesn’t want to use a CRM. Hire a trainer if you need someone to hold you coach you along as you adjust.

Hard to get people to come back – focus on providing the highest value as possible in the first interaction and you probably won’t have this problem. If they don’t come back maybe you solved their problem and so you should make sure they’re on your newsletter list and maybe you’ll get some referrals.

It’s transactional – the nature of the fee charged isn’t what makes it a transaction or a relationship, it’s how they feel about you and how you treat them that does.

Hard to scale – You can hire a paraplanner to work for you just as law firms hire paralegals. The benefits of scalability are exaggerated so that management consultants can sell you packages.

How does an hourly financial advisor track their time?

Rick uses his iPhone but I’ve also heard advisors say they use:

-

- Excel spreadsheets

-

- Paymo

-

- Harvest

-

- Toggl

-

- Clockify

-

- QB Essentials has a built in timekeeping system where you can track/enter time by client/project and then add that time to invoices.

-

- ClickTime

-

- GetMyTime

Note, I have not used any of these applications other than MS Excel, and am not endorsing any such application.

But won’t I make less money?

According to Rick, he has a long list of clients waiting to work with him because there is such a short supply of advisors who charge an hourly fee and a large demand from clients who seek this service. However, it should be noted that Rick has 30 plus years of experience and a podcast with over 1MM views.

It’s realistic to say that if you don’t have a big referral base or a sound method of attracting new clients to your practice, you may conceivably make less money until that changes.

I made this resource sheet for advice only, flat, and hourly fee advisors. Please avail yourself of it if you are down with the movement.

What advice do you have for someone who wants to become an hourly financial advisor?

Rick says it’s scary, but it’s easier than you think and way more rewarding than doing it the other ways. If you’re a good advisor you can be successful as an hourly financial advisor.

Sara’s upshot on hourly financial advisors

What’d ya think of my blog on hourly financial advisors? Was this helpful?

If yes…

Join the Transparency Advisor Movement.

The Transparent Advisor Movement’s mission is to promote ideals of clarity, modesty, integrity, dignity, and client advocacy in all aspects of financial advice, with a special focus on Advice Only, Flat Fee, and Hourly service models. There is a special emphasis on clear disclosure of services and their related fees.

The Transparency Movement is the future of the industry – we welcome anyone who believes in our values to join us.

Join our next Transparent Advisor virtual meetup.

These meetups are free and the goal is to learn from each other about how to grow and manage a transparent practice for the benefit of clients.

Even if you can not make the meetup, or even attend in its entirety, please register for the replay and to be notified of the next one.

Or if you are looking to market yourself better…

- I am an outsourced CMO for companies who need regular, full service marketing – blogging, social media posts, newsletters, etc.

- I am an hourly consultant for those who just need one-time or recurring guidance

- People hire me as a ghostwriter to write content for a project fee

- I have a social media training program

- I have a book about what to say on LinkedIn messenger

Just letting ya know, in case you need me at some point.

-Sara G

See you in the next one!

-Sara G

Podcast transcript

0:00:00.3 SARA GRILLO, CFA: The other day, it hit me that the own systems in America, other than a um, where you pay more for making more… Our alimony, child support, and the IRS. So the point of this podcast is not to debate about which fee model, but instead, I’d rather talk about How do we provide higher value to clients… So let’s talk about that. Let’s talk about how to provide high value, and the person I have here today is an hourly financial planner, so my goal is to learn about this from someone who does this exceptionally well. Today, I have Rick Perry with me, who is an hourly advisor, a CFP charter holder, and the host of the Bogle heads podcast, which has over 1 million views.

0:01:32.5 SARA GRILLO, CFA: And we’re gonna talk about how to provide high value as an hourly financial planner. Rick, welcome to the show.

0:01:39.2 RICK FERRI, CFA: Thank you for having me, Sara. I appreciate you having me on today.

0:01:43.2 SARA GRILLO, CFA: So did I get that right? About your podcast, you have over a million views… I saw something about that on social media.

0:01:49.1 RICK FERRI, CFA: I do, I started the Bogleheads on investing podcast back in… Oh, about three years ago, a little over three years ago now. And my first guest was Jack Bogle, and that was a few months before he passed away, and then I do a new guest every month. And the podcast is sponsored by the John C. Bogle Center for financial literacy, which is a 501c3 non-profit organization. I happen to be the president of that right now, and we have a lot of things going on with the both ads, including a conference coming up in Chicago next October, and it’s all non-profit and no one makes any money from it, and it’s just to try to spread the word about getting your fear shake on Wall Street.

0:02:41.4 SARA GRILLO, CFA: Yes. Well, that is great. Just gonna ask you about this because I know a lot of advisors out there are trying to do the same thing, they’re starting podcasts or they’re trying to kinda get the word out and get more visibility, what do you feel has allowed you to get an astounding amount of visibility in just three years.

0:03:03.2 RICK FERRI, CFA: Well, I think the bugle head’s name carries a lot of weight. I’ve been involved in that organization for 20 years, I’ve written a lot of books, so I’m very known in that organization, and then now I’m the President of the John C. Bogle, the bugle center, we call it. So I think that has a lot to do with getting people to begin to listening to the pieces, but I might tell you that… I think the first one I did it, I did it with Jack Bogle. I maybe had 5000 downloads and that was Jack Bogle, and so now we’re getting 30-35000 downloads a month, and it’s increasing every month, so it just takes time. It’s the slow build, if you would look at my listens over the last three and a half years, it’s just a very steady slow climb of putting out what I think is quality content and only doing one a month, and I think that with podcasts, the more you do of course, the faster it’ll ramp up, if you’re doing one a week, it ramps up a lot faster, but I only had time to do one a month because I do everything from start to finish, I don’t have any editors or anything, I literally pick the digest I do the recording, I do the editing, I do the marketing, I do everything front of back and I pay for all the…

0:04:27.7 RICK FERRI, CFA: All of it myself, as a matter of fact, because it’s like a non-profit, so it just takes time and you have to put on quick content and you have to have good editing, and it’ll build slowly… Like everything else in this business. It’s continuous, it has to be continuous. It has to… People have to anticipate that once a month or once a week, you’re gonna do a podcast and they’re gonna know the quality of the guests and know the quality of the recording, and it just takes time.

0:05:01.1 SARA GRILLO, CFA: And so also, I was reading that you were in the Marines… That you were a fighter pilot.

0:05:05.9 RICK FERRI, CFA: I was… So when I got out of college, I graduated from the University of Rhode Island with a degree in business back in 1980, and back then it was the worst recession you could possibly imagine, the unemployment rate was somewhere around 15% interest rate for sky high inflation was… Higher and there was no job height, you couldn’t get a job at a shoe store. Literally, but I ended up… I had always had an interest in the military anyway, I was an eagle scout back in the day when I was in Boy Scouts and so forth, so I always had an interest in the military, so what I did, once I joined the Marines, and they sent me to flight school, and I had never flown before, so that was interesting and did pretty well and got selected for advanced jet training, and next thing you know, I’m getting my wings and took a body… Two years from the time I went in the Marine Corp until the time I got my wings. In fact, I’m wearing them today, and it was a Navy wings because Marines go to Navy flight school, and I was the fighters for about six years, and then I went into the reserves for about 13 years.

0:06:19.9 RICK FERRI, CFA: I ended up retiring in 2000.

0:06:24.0 SARA GRILLO, CFA: Well, thank you for your service, and just one thing I’m sure of how much did they train you before they have you fly the plane?

0:06:33.0 RICK FERRI, CFA: Well, there’s a lot of steps to it. I think that they… They first go through all of the testing, it’s psychological testing, it’s obviously medical, and it’s a whole lot of testing before they even let you get into an airplane, and then you have to go through a whole battery of education… They have all of these modules that you do on aviation and weather and flight rules and all kinds of stuff, and it’s just one after another after another, and you have to pass all of these things, and then they start training you, it takes about… Well, the marines, it’s a little bit longer because you have to go to two different schools as a Marine before we end up going to flight skills, it probably took me before I actually got in an airplane… Almost a year of being in the military, in the Marine Corps. And then the flight school itself was a total… There was three different phases of it, but it was probably, I’d say about a year and a half long before you… They turn over the keys and give you a wings and say, You know, here’s a jet, go fly.

0:07:46.4 SARA GRILLO, CFA: Well, one of the reasons I’m curious about that, and by the way, for those who have been following this podcast for a while or following my writings, you may know that I’m definitely scared of heights. When I go to an airport, I have to just talk to anybody I see to take my mind off of the fact that I’m about to get off… Get on a plane and I’m like, I’m not crazy. I’m not… So the reason that I’m talking about this because to be a pilot that takes such a high degree of skill, and it’s kind of rare that you see someone that is successful pilot and has done this, and that’s really what we’re gonna talk about today is skill, having skill as a financial advisor, because I would… From my observation in the industry, what I’ve seen is that throughout its history, value has not often been tied to the skill of the advisor, but instead it’s been linked to a lot of times the AM or the performance or the products that the advisor tells… And I’m seeing that there’s a little bit of a de-linking that’s happening where with more technology and more accessibility to information, investors and clients are wanting more, and so that’s really the heart of what we’re gonna talk about today, is how do you deliver value as an advisor, because I think this is something that a lot of advisors have a problem articulating is what is the value that I deliver to…

0:09:24.2 SARA GRILLO, CFA: You’re an hourly advisor? No, yes. Okay, but before you were a… About your history?

0:09:37.0 RICK FERRI, CFA: Well, in 1988, when I left active duty in the Marines, I went to work as a broker for Kidder Peabody, which was kind of a boutique brokerage firm back in the day, a very quality company, and back then in the 1980s, brokers were…

0:09:55.1 SARA GRILLO, CFA: That’s what it was.

0:09:56.4 RICK FERRI, CFA: That’s what it was. To me, I didn’t know, but I thought that brokers were analysts that analyzed investments and make good investment decisions for their clients, and the clients do well, and the firm does well, and then me as the advisor, the broker, if you will, does well, and I thought that’s what it was all about, and I went to work in the brokerage industry, and you got a broker boot camp, that’s what they called it back then, and it was a little bit of what you see on the movies, the Wolf of Wall Street… The Movie Wall Street, it was a hard core sales… You would use the lines like, Well, you do try to sell somebody on the very first phone call, I mean you were trying to sell them a thousand shares of stock and 2000 shares of whatever the company was pushing at the time, then this didn’t seem to me to be, I don’t know, I was a little odd for me because I thought, Where is the research… Were supposed to be digging into balance sheets and income statements and asking clients a lot of questions about their around the answer was No, you’re supposed to sell them what the firm wants you to sell…

0:11:12.8 RICK FERRI, CFA: Well, I ended up using… Instead of me going out of doing that, I manage the clients fixed income portfolios and corporate bonds, just plans, I would actually build on ladders for the clients, but then I’d used money managers, stock money managers to go out and put together stock portfolios for the clients and these dock money managers all had something called the charter financial analyst charter, and so I said I should get that. So I did, I went out and I took the three exams and I passed and I became a charter financial analyst chart, but then I went on a designation. CFA designation, correct. Yeah, I did that early in the 1990s, that I had some understanding of portfolio management after allows in the investment industry, it seemed to me I should have some understanding, and it was odd that the firm that I worked for torpedo didn’t require any training at all, except you know what they wanted you to have. And so I went out on my own and I did this, and then I switched firms, I went to Smith Barney after five years, hitters broke up and sold off in pieces, and I went to Smith Barney and at MIT Barney, when I finished my charter Financial Analyst designation, I ended up…

0:12:32.4 RICK FERRI, CFA: It doesn’t need me as a portfolio manager, but then I went… I got my Master’s of science and finance where I continue to study and started getting into active management versus passive management and indexing and so forth, and benchmarking and a lot of different

0:12:47.1 SARA GRILLO, CFA: Things. At this point, are you… I mean, you have an established book, by this point.

0:12:53.2 RICK FERRI, CFA: I… I do, I have an established book. I gained clientele, I happened to do well with people who are very interested in investing, they weren’t just turning their money over to people there, rarely interested in investing, and I was going through all of this, so I sort of connected very well with the people who were very interested in getting into the weeds of analysis and a webcast.

0:13:15.2 SARA GRILLO, CFA: The financial advisors can’t stand clients like that. Well, that’s too, with the engineers and attorneys.

0:13:24.0 RICK FERRI, CFA: A lot of engineers, a lot of positions, business owners, and they were just more in-tuned with what was going on if you want… Yeah.

0:13:34.4 SARA GRILLO, CFA: That’s not in your money, you have a full-blown practice at this point, you’re not just selling on the phones anymore…

0:13:40.8 RICK FERRI, CFA: No, no, that’s correct. I was managing their money in

0:13:44.2 SARA GRILLO, CFA: The attire you hybrid or A and M.

0:13:47.6 RICK FERRI, CFA: Well, I was half and half because there the bond side was commission, I was just rolling bonds, they were built a bond ladder and then just roll the bonds when they matured, so that was a commission business, and then on the equity side, I was using money managers and then, I’m sorry, mutual funds or… No, no, it was actually individual securities, so separately managed to tie… Managing, yeah, correct. They didn’t call them as back then, but they were separately managed it on the same thing, and they used to wonder what I would call the RAP FERA and you gonna be taken back a little bit, but the fees on these things with 3%… Now, that was pretty high in charge 3%, but we could discount it down to 225, so if you can imagine… That was a high AUM fee. But that’s what it was. I was in a Humvee, and what I did though was I really monitored very, very closely the performance of these advisors and these managers, and realize that very few of them are even coming close to the performance of the benchmark, and I would create the benchmark… I got very much into benchmarking and indexing and index…

0:14:59.8 RICK FERRI, CFA: Indexes as benchmarks on index… A stock index is international India. I was very much into that. And so I was looking at these managers and comparing them, the value and growth indexes came out during this period of time, so I was using them to do analysis to see whether or not they were outperforming the index that I chose and they weren’t… They were significantly under-performed by a lot, it was a lot… And this is where I, in 1996, discovered Jack Vogel and Vanguard and index funds. I had my epiphany, my aha moment, and I said, Look at these managers. Can’t do it. They’re not doing it, they’re not outperforming. I’m just gonna start using index funds, which didn’t go very well with the brokerage model at the time, because there was no money in it. To do that.

0:15:53.2 SARA GRILLO, CFA: There was no money in it.

0:15:56.1 RICK FERRI, CFA: No, there was no money in it. I was using what I could, which were SPY, the S and P 500 by Andy, the S and P 400 mid cap, and those were the only two exchange faded funds that they had available, but working in a brokerage firm, you can have access to anything else. You can have access to Vanguard funds or index funds, because they wouldn’t pay the brokerage company marketing fees and they wouldn’t pay 12 B1 fees. Mean Vanguard wasn’t gonna do it. So we had no access. And that’s when I made the decision to leave the brokerage industry and start my own RIA, and that was in 1999. So I did, I left and started my own RIA at the time.

0:16:41.3 SARA GRILLO, CFA: What was the response from your clients when you said that…

0:16:46.4 RICK FERRI, CFA: No positive role. Again, they would have been following me and kinda watching me as I’ve been going through this evolution over about a 10-year period of time, and they were very much up to speed on where I was going and why I was going there, and they all… When you move from the brokerage to start your own RIA, about 80% of the clients will go with you, 80%. This is if you have a relationship with them. I sound the same thing, if you go from one brokerage firm to another, about 80% move with you… So I had done one move from one company to another, and 80% of the clients at 80% of the assets came with me… I just say 80% of the assets, not so much the clients because you tend to… A lot of the little clients behind and you take the bigger clients, it’s what you do. And when I left the brokerage industry and went, became an RIA, I took 80% of the assets with me and moved them over to Charles Schwab, which was my custodian and started doing a low fee advisory shop now as Lothian was very different in time using Vanguard and using, at that time, Dimensional Fund Advisors, some of their funds and a few things that look like index funds, be a weren’t index funds, and by my fee that I charge them was only a quarter over percent, so I recharging one quarter of the typical 1% management fee

0:18:08.9 SARA GRILLO, CFA: You… So that’s a huge delta from what your clients were being charged at when you were back at our…

0:18:16.6 RICK FERRI, CFA: So they immediately… They immediately got… Just from that, they immediately got about a 1% better return on their portfolios, but why did I get the one quarter percent fee from… Well, it came from the mutual fund industry where if you put a million dollars, say with American Funds as a fun company, you take a client, a million dollar Ira roll over and you put it into American funds and you divide it up between the Euro-Pacific fund Growth Fund of America and so forth. It’s a million dollars all going to that one fun company, so you don’t get a commission on that, the clients aren’t charged a commission to get in a front-end load, but you do get a trailing 12-1 fee. That’s how you get paid. So on a million dollars, you get paid 20500 a year, which is 25 basis points, and this is where I came up with the 25-025% fee only I wasn’t using American Funds, I was using index funds, and that’s how I came up with that fee and it worked very well actually. It was very successful. So it was really the first very low, a um, the RIA in existence at the time.

0:19:28.9 SARA GRILLO, CFA: Okay, so what happens after that? So this is like late 90s, early 2000s, started your own from… Okay, so now we’re in 2022. How did we get… What’s happened over the last 20 years?

0:19:42.2 RICK FERRI, CFA: Well, we grew very rapidly, and I grew… It was just me working out of my living room, much like I’m doing now, and we grew every rapidly I say we because they had to bring on a junior partner, and we expanded to about a billion and a half dollars, I was then in the process of selling out to this junior partner when we ran into some legal problems, him and I… And I ended up buying him out, and then I got bought out by a private equity investor right after that, so it was boom, boom. Two transactions, and that was it. I was ready to leave the AUM industry though. I was kind of almost beyond that in a way, there were so many good things coming out, like Vanguard had come out with their PAs program that was only charging 3%, and betterment had come out with a 025% program. Well, either a lot of other people were doing loyalty management, now it started to pick up steam, and I was ready to step away from the AUM model and do more advising because when you’re in a um manager, you’re not advising.

0:20:53.5 RICK FERRI, CFA: You’re thinking Gables, gather assets, gather assets, that’s what you’re thinking and get these assets invested and charge the fee, and then go to the next person and do the same thing. And go to the next person, do the same thing. It’s all your number… How much are you managing it? That’s what it was all about with a um, it wasn’t about actually advising people, and so I was really… A little narrative even now. That’s true. I… Then when I left, I had a non-compete. And then when the non-compete was over with, I said, Now I’m going to go back to doing what I think I’m good at. Well, I thought it was good at managing money and all of that, and everybody did well because the fees were low, like Oglala says cost matter, and that’s true in the advisor side as well, but when you’re managing money… So I decided I was just going to do an hourly model, I’ve been friends with Sheryl Garrett for many, many years, and I was very interested in her model with the Garter financial planners, and I’m not a financial planner by the way, but I do a lot of financial planning, even though I’m not a financial planner.

0:22:04.0 RICK FERRI, CFA: And so I do a lot with clients with investing, taxes, retirement planning, but when it comes to some of the other things like health insurance or estate planning, I’m not that good at that, and I’ll… I’ll do a little bit about that, but basically I tell them they need to speak to it in estate planning attorney or in the insurance side, that we need to speak to somebody who is more knowledgeable about healthcare and self-use, there’s certain parts of financial planning that I don’t get involved in what… If you’re talking about taxes, you’re talking about investing, retirement planning, I’m all very, very good at that. Integrating Social Security, Medicare, ermine, all of these things that go along with retirement, I’m very good at… So this is what I work with clients on. And I get paid by the hour. Yeah.

0:22:57.5 SARA GRILLO, CFA: So you’re saying the Cheryl, Gary influenced you in that direction? Yeah.

0:23:05.7 RICK FERRI, CFA: Absolutely, I Road, I’m sorry.

0:23:11.0 SARA GRILLO, CFA: To my knowledge, there are a ton of hourly advisors out there, there are not… There are not in

0:23:19.5 RICK FERRI, CFA: Our hope, I’d say our hope, because there are few and they’re growing. Our hope is that they’re more advisors realize that this is really a viable business, you could make just as much money as an advisor doing just advising, then you can managing money, and it’s hard to step out of the money management role. Give that up to turn it over to somebody else, if you will, and just become an advisor, but it’s much more rewarding, I think, because now as soon as you do that, you are lifted, in other words, there’s a lifting, if you will, of the pressure on you to build a um… And you could actually… You listen to yourself talk to these clients now as an hourly advisor, and you’re saying things that you probably would have never said As an AUM advisor because your forum was to build a… Um, your focus now is on what does the client need, and what should we be doing to help the client, and no matter where it takes you, this is what… This is what your focus is. You’re not trying to move money from UBS over the Vanguard… I’m at UBS over to Schwab or Fidelity, so that you can manage it.

0:24:44.0 RICK FERRI, CFA: That’s no longer the focus. The focus now is, I don’t really care where you have your money, let’s do what you should be doing with it, and I’m not… My compensation, it’s not based on a product anymore, it’s based on advice, now it’s different, very different.

0:25:02.6 SARA GRILLO, CFA: So do you have a discretion on the accounts…

0:25:08.6 RICK FERRI, CFA: No, no. Not a law, no. I talk with the clients, they send me other statements, I do an analysis for them, then I get on the phone with them, we talk for a couple of hours, this is a new client, I call this a portfolio or a second opinion at the end of that two-hour call after we go over everything, I might spend the first hour and a half talking with them about their goals, their family, estate planning, taxes, social security, Medicare, health care, holding on to pay for health care, the types of accounts that they have, distributions from retirement and then actually the last 30 minutes as we’re talking about the investments in the portfolio, but at the end of that two-hour call, I’ll write up a letter, it might be three, four or five pages long on all the things that we talked about and all the recommendations that I had, and then I send that to them and I get paid 995 for that 95 flat fee for that. And then that’s it pretty much done, if they implement it on their own, if they have questions, they can email me and I just answer them as needed, I don’t charge for that, I…

0:26:12.7 RICK FERRI, CFA: And a year or two or three, they wanna come back for a check-up or they have more questions, I just charge an hourly fee for that, and I charge 450 an hour, and I’d say… Maybe after a year or two or three, maybe 20% come back, I imagine. I’ve been doing this for three years, I imagine as I move along, maybe half the people will come back for a check-up, but quite frankly, after I’m done with that portfolio or second opinion, that’s it, it’s a one-time package deal, and there’s no obligation… I don’t run a dentist chair where I’m trying to schedule them, you’re in advance or six months ago, I don’t do anything like that, if they want the help, they just get back on my schedule and I’ll get up to speed by… We’re reviewing everything that I have in my files on them, and then I get back on the phone with them and talk with them for a one, 30 minutes might be 45, might be an hour. You know, I probate that our fees, but I stay pretty busy, and so I do one new client a day, and then I do generally an hour to an hour and a half of an existing client, and you look at it and that’s 1500 a day.

0:27:20.6 RICK FERRI, CFA: Revenue coming in, and you multiply that times 20 days. You’re talking 30000 a month, let’s call it 10 months. That’s 300000 a year. That’s very, very easily done. And it’s just all hourly, there’s no way you win there at all, no product sales.

0:27:43.1 SARA GRILLO, CFA: But how do you get the one new client today, I mean, you have your podcast… Well, that’s marketing.

0:27:50.2 RICK FERRI, CFA: All the devices have to market marketing is continuous, you can’t just hang a shingle out there and they will come, that’s not what… You gotta be out there. I’ve read many books, I’ve written articles, I do the podcast, and I’m out there, and I’ve been out there for 25 years, and so I’ve built up a following and people have come… And that’s how I get my clients, but I have to tell you, even people who are new to this who are just kind of getting started, they’re building a clientele, I’ve helped fellow by the name of John Lusk in get started last year and building… He’s building up my clientele, he’s staying busy, he’s booking clients now, it’s not as much as I am, but he’ll get there and there were other people as well who were just all booked up, and it’s very hard to find somebody who has the time to work with it, but, but there’s a real shortage of people like myself and John and other folks out there who are doing this pretty much difficult to get on somebody’s schedule, it really is, I’m booked up for these portfolios, second opinions, all the way to the end of the summer and I have about 100 people on a waiting list for…

0:29:00.9 RICK FERRI, CFA: At the end of the summer, when I open up my calendar for the fall, I have about 100 people on the waiting list already, so I’m gonna be booked up as soon as I open up my calendar… At the end of the summer for the fall, I’ll be booked up through December for the whole year, I could literally book up to the whole year right now if I opened up the calendar, but I attained that image booked up 10 months in advance for these and that’s the way it is. What is… How much demand there is, what this out there.

0:29:31.2 SARA GRILLO, CFA: Because you are in the small number or advisors who have chosen to structure your practice this way… Correct. Yes, but the demand is overwhelming, it… I can’t

0:29:47.0 RICK FERRI, CFA: Describe to you how overwhelming the demand is for whether this service… It’s there, but that’s difficult for the advisors to accept it and to this decision that they’re gonna go this direction, it really, really is… Again, I’ve been in the business for 35 years now, it’s hard. It was hard for me to leave up the broker, give up the brokerage industry and start an RIA because they had to give up trailing commissions, and it was quite a bit of trailing commissions that I gave up, but I couldn’t do that when I became an AM only RIA. I wasn’t a dual registered Ria, so I had to give up the trailing commission, it was difficult to do that, but it was difficult to give up that really nice paycheck from AUM to turn around and start an hourly business from scratch. It’s difficult, it is. It’s hard to make that decision to do that. But I mean, I’ve been fortunate I’ve been able to do it, and I think this can do it as well, and I do have inquiries from advisors all the time saying, What if I wanted to do what you’re doing, but right now I’m doing a um…

0:30:54.0 RICK FERRI, CFA: Well, first you have to find somebody to take over the management of the client’s portfolios. And there are money management companies that’ll do that and you can stay as the financial advisor on the account, just advising the client while the other company is actually doing the behind the scenes portfolio management, but you’re not actually doing it anymore.

0:31:13.2 SARA GRILLO, CFA: Great, that’s important. Can we just pause it there for in… Could you give some examples of such companies…

0:31:20.7 RICK FERRI, CFA: Well, the fellow that I use is I used to work for me. His name is Ken carbo and its Liberty Capital Management up in Birmingham. He was my portfolio manager at the company that I had for more than 10 years, and now he went out and he started his… White has his own company, is managing about 500 million, but all he does is portfolio management, they don’t do financial planning, they are investment people, portfolio management people to…

0:31:45.1 SARA GRILLO, CFA: We get some people out.

0:31:46.3 RICK FERRI, CFA: His company, he… His company, any charges the charges, the clients that I sent to them, he charges them a quarter of a percent per year management fee, which is what I negotiated for the clients that you know, I sent to him, but he’ll do that for any advisor pretty much our goal charge a flat fee. In other words, a lay instead, in other words, if you wanted to do a flat fee instead of doing a um, the, he would do a flat fee, so I can’t speak to what inwards would it be? Probably if you had 5 million, 6 million, it might be 60 or 70 or 80000 a year. I really can’t speak to what it would be ’cause that’s between the client.

0:32:32.9 SARA GRILLO, CFA: But that’s much less than what it would be… Oh sure.

0:32:35.8 RICK FERRI, CFA: It’s a lot less because his role in this thing is to manage the investment portfolio now, if the client keeps me involved, then I’ll speak with the client also, and if Ken carbo wants my advice, I charge him also, in full disclosure, he has hired me as an advisor to down the investment advisory committee that he had, so he pays me my fee for just advising him, and I have some other advisors out there that are doing that also, but… That’s one option. There are many other people, I send a lot of people to Van gardens as a lot of people to pass, because paisa portfolio

0:33:20.3 SARA GRILLO, CFA: Maybe…

0:33:21.1 RICK FERRI, CFA: I don’t really send clients to bet not. I like better, and I like it better when John Stein was there. But he’s not there anymore. I’ve got a lot of respect for what John did, her or portfolios are just too complicated for me, they just… They just have too much stuff in the airport. Follows and say anything with, Well, friend, I like Andy red life and what you did over at World front now, it’s part of UBS, but there’s just too much stuff going on in their portfolios. It’s too complex. I like simplicity. And so Vanguard is very simple. They’re making it more complex now, but they used to use just for funds, so I like that. So I’ll send people the PAs and so forth. Betterment? No, not ever. It’s just too complicated, and I’ve told them that too, that it’s nothing new to those folks. I’ve told them many times, I have this thing, complexity for job security, right? Which means advisors make things… The portfolio is too complex because it gives them job security… I don’t like that, there’s no reason to do that. Over-diversification, it’s not diverse cation, it’s complexity for job security, I mean, when you take a…

0:34:31.2 RICK FERRI, CFA: I call it the Humpty Dumpty strategy, and it’s actually Arians last name, but he has a great cartoon out there, I put it up on Twitter, and basically it has this picture of Humpty Dumpty getting pushed off a wall by a money manager and Humpty Dumpty breaks into a bunch of pieces, and then the money manager comes to long close all back together in charges 1% AUM for it. In other words.

0:34:53.3 SARA GRILLO, CFA: You can see that the other day.

0:34:56.1 RICK FERRI, CFA: It’s a great cartoon, a wonderful… And it just perfectly captures what’s going on in the industry complexity for job security, and it is… You know, you don’t need that. You just need a few good funds, a total stock market, us total International, a couple of bond funds, you really don’t need a complex portfolio, Vanguard has this figured out, Bacardi collecting 30 basis points management fee, and people are getting a very simple portfolio, so it’s not the portfolio, it’s not the portfolio that people are concerned about, you don’t need to make things complex for clients, you don’t need to not lock the client into something, that when they look at the portfolio, they say, Oh, there’s so many things here, I can’t figure this odious, leave it up to you now. That’s not fair. It’s not fair to the client, I mean, if it’s… You don’t need to take US stock market and divide it into growth value, large cap, small cap, mid-cap, and six different funds and break it all apart and then put it back together as a total stock market fund, just keep it as a total stock market fund it’s much simpler.

0:35:58.3 RICK FERRI, CFA: What’s more tax efficient? Lower cost, less complicated. And clients appreciate that they’re still gonna pay you because they want you to tell them what’s in their best interest in doing a simple portfolio is in their best interest, and this whole idea of complexity for the sake of job security is going the wrong direction in my opinion.

0:36:20.7 SARA GRILLO, CFA: So now, when… So you mentioned that you charged… Was 450 an hour? Did you say, Forgive me five5 an hour. Okay, how do you come up with that number?

0:36:34.2 RICK FERRI, CFA: I asked Alan Roth how much he was charging, Allan Roth has another financial planner, and he said he was charging 450 an hour, and I figured if Allen was charging that I should be able to get that to…

0:36:44.2 SARA GRILLO, CFA: Right. And then you’re two hours… That’s a flat fee.

0:36:51.1 RICK FERRI, CFA: Yeah, so the 995 was my creation. I looked at it and I said, Okay, how long is it gonna take me to do one of these portfolio or second opinions? And it takes me about four hours, so I work off of about 30 minutes of looking at all the information and getting it all in a format that I understand, that I can see what the client has and where they have… It takes him about 30 minutes to do that two-hour conversation on the phone with a client, and then about an hour and a half after that to write up the letter because all the letters are handwritten, so it’s a four-hour turnover. So I’m getting up early, about 250 an hour for that, but that’s okay, ’cause those are new clients now, when they come back, I charge 450 an hour because what I really… It’s not really 4-50 because I have to go back into their stuff and I have to get back up to speed on what we talked about last time, and I don’t charge them for any of that time. And then when I get them on the phone, if it’s just 30 minutes and I get 225 for that.

0:37:56.3 RICK FERRI, CFA: So it’s really not… Small ends up being about 250 hours what I really get. So that’s really what my fee is, if you wanna look at it from beginning to end with each client, from the paperwork all the way through to going on to the next thing, it really ends up being in about 250 an hour.

0:38:19.6 SARA GRILLO, CFA: This is so interesting, and thank you very much, Rick, because this is something that I’ve been speaking about in the such resistance, but this is gonna help me in my future writings on this. One of the things that I think about a lot is the degree to which the industry, in many cases, doesn’t handle smaller portfolios appropriately Sue, and because I see often this 15% for accounts under 1 million. And if you look at what the impact is on a portfolio, a small portfolio over time of a fee that large, it’s astronomically expensive. Absolutely. Okay, Rick, can you tell me about what your typical clients portfolios tend to look like, are these… Are these larger portfolios at a smaller portfolio

0:39:11.2 RICK FERRI, CFA: Trays… I’ll give you the range. My smallest portfolio was negative 300000. Now, why do I say that? ’cause they were 300000 in debt. He was coming off, I was in residency of a doctor in residency, but he wanted to learn to invest the right way and do things the right way, right from the start. He had a 300000 in student loans. He was just getting started with a 4 or 3 at the hospital he was working at. We also had a 457, maybe you had maybe had 10000, 11000 actually invested. So yeah, I charged them in 995 and we did the portfolio second opinion, and now he’s got a plan and go forward, and with this in a not.

0:39:55.1 SARA GRILLO, CFA: Okay, but this is the kind of a scenario, Rick, the financial advisors would say, I don’t want anything to do with this person, I can put him on my wait list, I could put him on my mailing list, but I’m not interested in this type of client, and this is a radiologist earning 300000 or more a year. So

0:40:18.4 RICK FERRI, CFA: Much radiologist, radio. But anyway, go ahead.

0:40:23.3 SARA GRILLO, CFA: You know what I’m saying? This is such a great opportunity for the advisors that can do things a little bit differently and not have to have it tied to a… I mean, look at what you’re missing, whereas when this person gets out of debt, which is probably gonna be in not too long amount of time… Right.

0:40:42.1 RICK FERRI, CFA: Long forgiveness after 10 years. But okay, advisors who put this person on a wait list… Well, they might be on your wait list, but that you as the advisor, I’m not on their weight list, if you’re not gonna take care of their needs now when they’re contacting you, you are out Toomey, could go ahead and put them on your waitlist and send them whatever emails you want every six months and contact them every year and say, How much money do you have now, but they’re not gonna work with you, not gonna work with you because you rejected them when they needed you, and so it’s…

0:41:19.4 SARA GRILLO, CFA: Okay, and you know what else is more to the person working at the start-up that doesn’t have the stock options yet, or it has it, but it hasn’t gone public and so… Or whatever, or not that much money. And that’s the same thing where they have this joke in Silicon Valley that like when they see people sitting in the lobby with the suits on, they know… It’s a Wall Street person, you know what I mean? It’s because there’s such a rush when the company finally IPOS and it’s like, Well, imagine if 10 years before that you had been the advisor that they trusted that they’re talking to and then… Sure

0:42:01.0 RICK FERRI, CFA: Happens all the time with me. I mean, the people who come back to me, Hey, I did sell my company, we did IPO, what do I do? How do I handle all this? Do… Well, sure, it happens all the time. So by the way, so my smallest client is 300, give 300 million, the largest client was about 100 million, and I have several clients that are over 50 million, but it doesn’t matter, I don’t get the same amount of… I get the same amount of money, so it makes no difference to me whether I’m working with somebody who’s got 50 million or 50000, it doesn’t make any difference.

0:42:34.8 SARA GRILLO, CFA: Okay, Rick, so let’s talk about the client with 50 million, that person is working with one of these portfolio management firms that you’ve referred them to… No, or whoever they’re working with.

0:42:48.3 RICK FERRI, CFA: Generally, generally, they come to me, either they have been self-managing their portfolio their whole life, or maybe they were working with a Goldman Sachs or somebody like that, or maybe a money management company, but generally… And they have come to the light, they have realized that they’re paying way too much and it’s all about no smoking mirrors in many ways, complexity for the sake of job security and things are going over it before, and they’ve had the epiphany. They’re ready now to make a change, and so I’ll either… When they’ve been doing it themselves and they’ve already been managing their own portfolios and sort of the bog headway, it’s more of a validation or confirmation of what they’re doing, and when they come from another advisor and it’s this complexity for the sake of job security portfolio, there’s something Dumpty portfolio that the advisor put together, it’s a restructuring, I have to restructure things and make them simpler so that they can manage it, so the idea is get them to the point, if they’re already doing it, it is validated and clean it up a little bit if needed to trim around the edges and so forth, but if they are just…

0:44:03.3 RICK FERRI, CFA: They just converted and they have this really, really messy portfolio and they always come that way, they’re just an absolute mess of stuff and you gotta take that and you gotta bring it down to something that they can manage. And sometimes that takes a while for them to be able to do it, but I do turn it up now, those people who say… Those are the people who will say, I don’t really wanna do this myself. And then I’ll say, Okay, well, I can refer you to somebody who can do this for you. But do you have to pay them a fee? And here’s the names of a few people who you may wanna talk with about doing that, and then I’ll give him the names of some people. So depending on what they wanna do.

0:44:46.0 SARA GRILLO, CFA: Okay, so a lot of the time when I talk about… So first all, do you use a time tracking out…

0:44:55.0 RICK FERRI, CFA: Yeah, schools, an iPhone, iPhone right here. Basically, when I make all my calls on my iPhone and I could track them out of time I’m spending on the phone with them, like I said, I only… On the hour Lea stuff, I’m only charging for the amount of time I’m actually speaking with somebody, but I know it’s like double that the amount of time that I actually have to put in. So it’s like a… Say, I charge 450 an hour for the amount of time I’m actually speaking with them on the phone, but in fact, it’s actually twice that amount of time that I put in, and the same thing with the portfolio… Second opinion, I charge it in the 995, but it includes the time beforehand to prepare and then the time afterwards to write the letter, so my track time tracking app is just my phone, I can see to the minute how much time you spent on a call.

0:45:49.0 SARA GRILLO, CFA: So people are you… Some advisors will argue that this makes the client have to pay more, cloth have to pay more than it cost more at the most stressful times of their life, like when they’re getting a divorce or they’ve had a major life change, and for that reason, I don’t know how…

0:46:10.1 RICK FERRI, CFA: I really don’t know how… I do Howlett claim. I mean, how… How much time do you need to spend with somebody who’s going through this major life change, maybe they’re retiring selling their business, maybe they’re getting divorced, how much actual time does the advisor need to speak with them and help them hit an hour, maybe two hours, maybe

0:46:35.3 SARA GRILLO, CFA: A $000, or you’re an excellent communicator, you have a podcast, you’ve been in the business 35 years, you probably have somewhat of an idea of how to handle clients and how to answer questions, and a lot of the situations you’ve heard before, and you know how to handle it… But that might not be the case for somebody that’s a little bit less experience, let’s say there’s someone get into business five to 10 years and the client comes to them and says, You know, I’m getting divorced and I don’t know how to… I don’t know how to handle… How to split this up? Do I need a Quadra or this or that? You just can see what I’m saying, not everyone’s as good a communicator, I think… I think that’s important because when you’re talking about time and you’re talking about charging people for time, I do think the advisor has to be able to be in command of these kinds of situations, so that doesn’t… The cost don’t get out of control for the client.

0:47:33.5 RICK FERRI, CFA: Well, that could be true for some advisors, but I do also think that there’s a lot of stuff that might happen that isn’t really necessary low, let’s run a Monte Carlo simulation model and see where this thing comes out, let’s do an optimization Here, fill out this 00 question questionnaire. A awful lot of stuff that you’re right, because of my experience, I just skip over all that stuff, it’s not… I don’t find it to be useful at all. And let’s just get down to the Metro, what really is important, but yeah, if advisors in their career will learn over time what’s important and what’s not important, I understand in that process, they might be spending more time with clients as the advisor learns than they need to but then again, I don’t think that the average advisor is charging 45 and either… My view.

0:48:34.0 SARA GRILLO, CFA: Right? What do you feel has been the most difficult thing to put this hourly model in place?

0:48:42.6 RICK FERRI, CFA: Oh, just telling people, I’m booked. That’s the most difficult thing. I can’t get to you, Sarah, I really like to work with you, but I really can’t put you on my calendar until November. So you got April, May, June, July, I go September over eight months from now as… When I can talk with you, I’m sorry, but I apologize, but it’s just, I’m just booked. That’s the hardest thing for me.

0:49:07.1 SARA GRILLO, CFA: Yeah. Okay, it, so thank you so much. I realized we’ve gone over on the time here, but this

0:49:12.9 RICK FERRI, CFA: Semester about the banging in the background, we got some people working here… Oh.

0:49:17.2 SARA GRILLO, CFA: Well, that’s okay. You know, I have four kids, so there today, but that they’re always on my podcast. Okay, great. What advice would you give to… Maybe not like a really 30-year veteran in the business, but someone that maybe is either starting out or is maybe, I would say early to middle stage financial advisor that wants to transition to this model or wants to start a practice with this model. What would you say to that person?

0:49:52.3 RICK FERRI, CFA: It’s scary. It really is. I mean, to make this transition, it’s hard now, I think that a lot of advisors who are really, truly advisors, I truly wanna be an advisor, that’s what they wanna do, that’s what their heart is in helping people advising people or doing portfolio management, because it’s sort of the way that they learn is what they were doing, but that’s really not what they wanna be doing, that… It is scary to make this transition, but it’s not as hard as you think… It is very rewarding. The clients do understand, it’s just you are your worst enemy and making this decision because you can be very successful at it, and if you’ve been successful prior to that doing whatever model it was that you were doing, you’re gonna be successful doing this hourly model. Okay, if you were not successful doing whatever what you were doing before, like AUM or commission, you just weren’t… Then this is gonna be a tough model for you too, because you probably weren’t very good at marketing, you may be very, very good at what you do, but you’re not good at bringing in clients, and if you’re good at bringing clients a good at marketing, you’re gonna be good no matter what model…

0:51:11.1 RICK FERRI, CFA: The model you use. You’re gonna be successful. And that’s really the key there. So if you’ve been successful as an AM advisor, you’re going to be successful as an hour the advisor, you will, and it’s just a scary move to make, but if you really feel your heart is into it, if you actually do do it a couple of years later, you’re gonna say, I don’t know why I didn’t do this years ago.

0:51:39.5 SARA GRILLO, CFA: So how can people contact you?

0:51:42.4 RICK FERRI, CFA: Rickey dot com, that’s my high website, and I answer all emails and if it’s an advise… If you just want to talk, I just basically say, Oh, let’s have a conversation. Now, I also have an advisor consulting business, it’s not very big, but I was talking about… Ken carve from Liberty, we got four or five different advisory firms that advise you and financial planners that I advise to, but again, I just charge the same hourly fee as I charge for clients, but most of the time I’ll speak with an advisor first conversation, or I don’t know how long… Sometimes we get into these conversations. If you and I are talking, this could be one of those conversations where you’re an advisor, you just asking me questions that I freely give you my advice, pro bono, what I think and that… Send you on your way. But if you want me to do more than that, you do some sort of a coaching, then it gets into our contract or an engagement letter, and I start charging for my time, but I’ve always been Freely, freely, freely giving advice, whether people want it or not, as you probably saw on Twitter.

0:53:02.7 SARA GRILLO, CFA: Yeah, well, thank you for mentioning that because I feel that there’s a lack of good guidance about how to transition to the hourly model, I mean, I know that there are some advisors doing it, but there’s all this resistance to it, so I’m really glad that you’re out there to support people who do wanna do it, and I’m hoping that this podcast will inspire people to consider it, but prior to, we’re kind of blocking it off in their minds, so thank you so much for being here. Rick, really appreciate it.

0:53:41.9 RICK FERRI, CFA: Well, like you said, I appreciate you having me on. 0:53:44.6 SARA GRILLO, CFA: Great, okay, everybody. So that’s it for now, I will see you in the next one. And please rate, review and subscribe to this show

Disclaimers

Podcast transcript may be altered from its original recording

Grillo Investment Management, LLC does not guarantee any specific level of performance, the success of any strategy that Grillo Investment Management, LLC may use or mention in any of its content, or the success of any program it may mention in any of its content.

Grillo Investment Management, LLC will strive to maintain current information however it may become out of date. Grillo Investment Management, LLC is under no obligation to advise users of subsequent changes to statements or information contained herein. This information is general in nature; for specific advice applicable to your current situation please contact a consultant or advisor.

Also, nothing in this podcast or blog can be interpreted as legal or compliance advice. For advise on such matters, contact a legal or compliance advisor.

I have no formalized business relationship with any of the firms listed on this hourly fee financial advisor list. This is not an endorsement of any particular company. Please conduct your own due diligence and come to your own decisions. Also, I am under no obligation to update this list and the conditions of service offered by these firms may change over time without being reflected here.

Music is Nice to You by the Vibe Tracks