I established this page to talk about marketing for flat, advice only, and hourly fee financial advisors in the hope that it can be a resource to support the transparent advisor movement within our industry.

Thanks for visiting me.

I am Sara Grillo, CFA and I’m declaring war on all forms of deception, manipulation, and other old-school, toxically controlling behaviors within financial advisor practices.

Marketing/practice management resources for transparent financial advisors

Right now these are the resources I can offer you as support. I plan on updating this as I gain more resources to share with you.

The Transparent Advisor Movement’s mission is to further the ideals of:

- Honesty

- Integrity,

- Humility,

- Fairness,

- Logic, and

- Advocacy

in all aspects of financial advice, with a special focus on Advice Only, Flat Fee, and Hourly service models. There is an emphasis on logical and clear disclosure of services and their related fees.

The Transparency Movement is the future of the industry – and those who join us are the ones who are called.

#1 Read these blogs

I put together a series of interviews and blogs about marketing and practice management for flat fee financial advisors, hourly financial planners, and advice only planners.

Here is the playlist – enjoy!

#2 Watch these videos

I have an entire YouTube playlist dedicated to this.

Watch these videos:

How to create a flat fee advisor website that ROCKS (tips + example )

Flat fee financial advisor biography: example. This rocks!

Flat fee & advice only financial advisor LinkedIn page tips

How to talk to reporters if you want to get tons of free PR

Advisor interviews:

#3 Get your SEO game right

First of all, please install Google Analytics and Google Search Console on your website. They are free tools. You can probably do it yourself, and if you can’t there are freelancers on Upwork that could probably do this in less than an hour. The reason you need these tools (and need to learn how to use them) is that your website can be a valuable tool for catching prospecting traffic.

Consumers are searching for flat fee, hourly, and advice only financial advisors. If you set up your website right, maybe you can come up in a search for some of these terms and get on their radar screen.

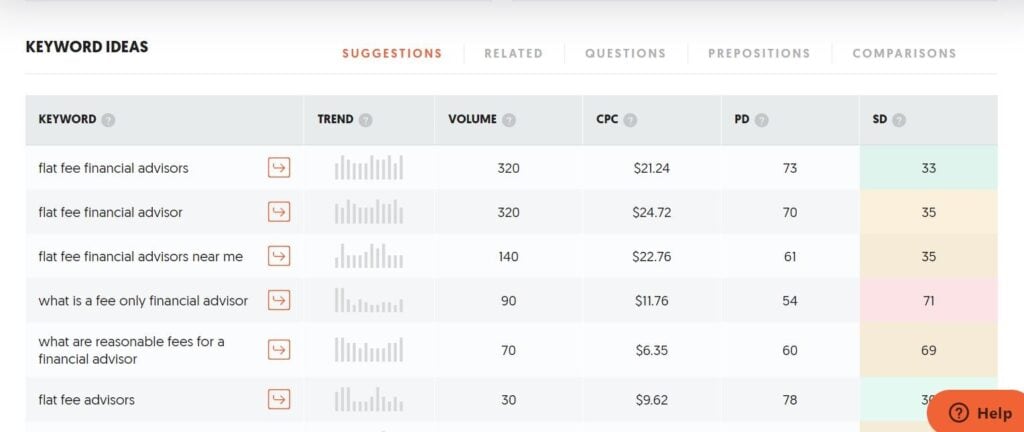

Check this out from Ubersuggest as of March 2022:

It’s basically saying that as of 3/17/22, when I researched this, that there are over 600 searches a month for terms related to “flat fee financial advisor.”

That’s fabulous!

It shows people are looking for planners like you online.

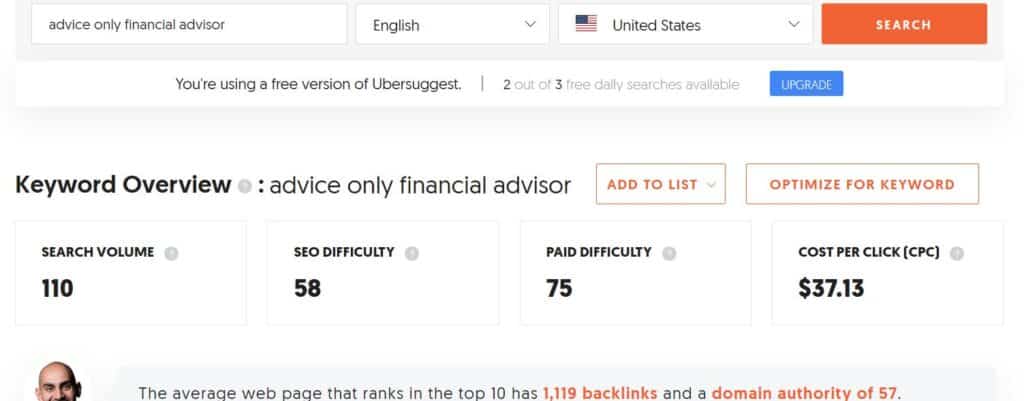

Also look at the search volume for the term “advice only financial advisor” as of April 7th, 2022, also from Ubersuggest. Not as high as for “flat fee financial advisor”, but there is some volume.

So, one of the things you want to do is try to grab as much of this traffic as you can while the getting is good! The keyword difficulty is low – still in the 30s. Get ’em now!

- I did this podcast talking about how to optimize your website for SEO.

- Also, Neil Patel has a fabulous blog about how to set up your blogs and website to get more traffic from Google. I’ve done quite a few of these myself and they’ve helped.

- Try to get some of the local searched by including keywords on your website such as “Flat fee financial advisor in ??? city”. It should be on the homepage up high before the folder. Example, “We are a flat fee advisor in Boise, Idaho serving local families and clients across the country.”

- Consider writing a blog entitled, “Questions to ask a flat fee advisor in ?? location.” See Patel’s tips above for SEO optimization of blogs.

- Same instructions as above if you are focused on a niche. “Flat fee advisor for veterinarians.” Or the likes.

#4 Get a Flat, advice only, or hourly fee advisor value proposition

Get your pricing clearly displayed and its benefits explained on your website.

- State that you charge flat or hourly fees clearly on the home page before the “fold” so they don’t have to scroll to see it

- Give it its own tab on the home page menu called “Fees”, “Pricing” or “How we get paid”

- Get a fee calculator so the viewer can compare what they would pay with you vs. what they would pay in AUM fees

Moreover, clearly explain what the benefits are of working with an advisor who charges flat or hourly fees, and tie that into your value proposition.

Example:

“We found that many of our clients needed us to advise on assets that were held away, such as bitcoin, real estate, or business interests. We set up our fees this way so we could include those assets into the planning which provides a more comprehensive view of the client’s total wealth including all assets and liabilities.”

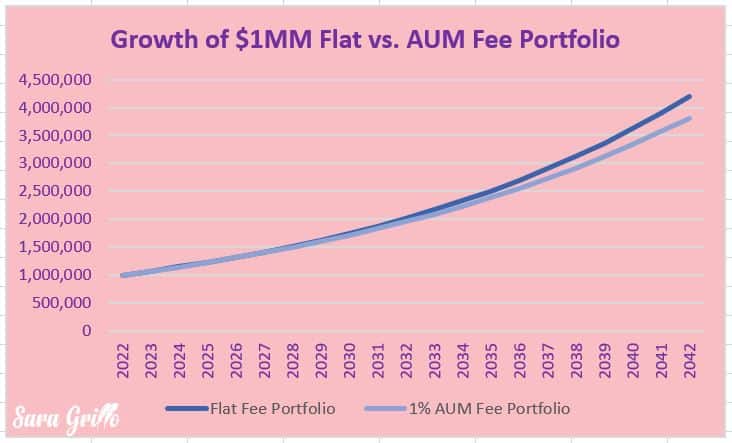

#5 Include graphic depictions of the differences

This isn’t the best graph in the world but it does show the basic differences between what a flat vs. AUM fee portfolio would hypothetically look like. The assumptions are basic (I’m sure you could do much better) but you can see the major point.

Notes: 1% fee on AUM, $10k annual flat fee, 8% annual nominal growth rate, fee debited at end of year, no withdrawals, contributions, or transaction costs, 20 year time horizon.

Projected growth of portfolio is entirely hypothetical; future performance is not guaranteed. This illustration does not include ongoing service, platform, product, and other miscellaneous costs; this may decease potential yearly and accumulated growth and/or fee savings . Actual portfolio growth may vary.

You can see there is quite a delta. The flat fee portfolio reaches $4.2MM while the 1% AUM portfolio only gets to $3.8MM.

What I’m trying to say here is that you don’t just have to use words, you can and also show the differences graphically where possible.

#6 Network with other flat, advice only, or hourly fee advisors

I’ve created a LinkedIn group where flat and hourly fee advisors can post discussions and chat amongst their peers. Please feel free to join it, and if you do so I please kindly ask that you observe group rules.

I have a monthly meetup over Zoom. Sign up for the next one here.

Here are lists of advisors you may want to meet and network with:

#7 Subscribe to Transparent Advisor Letter

Join my Transparent Advisors newsletter to be notified as future resources become available, and to receive my quarterly updates on marketing and practice management tips for flat and hourly fee financial advisors.

#8 Follow Transparent Advisor Movement on Instagram

Here is a page entirely devoted the transparency movement.

That’s all I’ve got for now!

Thanks for coming by. Please stay in touch and let me know how your mission is going!

-Sara G