I’m tired of these nonsense “top advisor” lists based on AUM or how many Twitter followers somebody has. I feel that to proclaim that somebody is a top advisor based on AUM or Twitter followers is an abridgement of morality, and it is my goal to overshadow any media voice that claims as such. So here’s a blog about some things that ethical financial advisors do in the hopes they will serve as an example of right behavior for the rest of the industry to follow.

For those of you who are new to my blog, my name is Sara. I am a CFA® charterholder and financial advisor marketing consultant. I have a weekly newsletter in which I talk about financial advisor lead generation topics which is best described as “fun and irreverent.” So please subscribe!

I am an irreverent and fun marketing consultant for financial advisors.

Ethics matter in financial advice!

Ethics matter.

If there were more examples of ethical financial advisor practices, then there would be more rightful actions taken by the industry as a whole. I wish I could say that this could be considered a “Top Ethical Advisor” list; however that wouldn’t be accurate.

The following case studies serve as examples of ethical actions taken by financial advisors. There’s nothing to say that these advisors are ethical in all aspects of their practice.

How I composed this blog

The examples below were researched based upon a questionnaire they filled out, their ADVs were checked, and they were questioned as to their responses. This is how I understand these advisors, to the best of my knowledge and capabilities, but the research is not ongoing. Their status could change at any point. You’ll have to do your own research to determine if these advisors really are ethical.

Also, I’m not endorsing anyone or recommending any financial advisor on this list. I want to be very clear that I was not paid to feature any of these advisors; no monetary relationship exists with any of them. Also, the examples in this list are not presented in any particular order relative to meaningfulness; this is not a ranked list, and the order is random.

And if you are considering hiring a financial advisor, please do your own research. This is not an endorsement of anyone mentioned here, and situations could change and not be reflected here. Also, there is selection bias inherent in this list. I did not interview all the hundreds of thousands of advisors out there, I conducted research using Google and posted on social media. So this is limited to those accessible to me. Again, conduct your own research; this list is intended to be a starting point but by no means is it exhaustive or conclusive.

Financial advisor ethics

So here’s my attempt to showcase some things that ethical financial advisors do in the hopes to drown out the voices in the media publishing crap financial advisor rankings highlighting those with the most AUM or Twitter followers. In one case, Investopedia named an advisor to one of the “top lists” who was banned for her non-disclosure of commissions earned in a Ponzi scheme.

Yup.

I mean, I just don’t know what else to say. It’s ludicrous.

Okay before I get fired up, let me move to to talking about some highly ethical things I’ve seen financial advisors do, so that we can focus our attention on increasing morality in wealth management.

#1 Clear fees, clearly disclosed on website

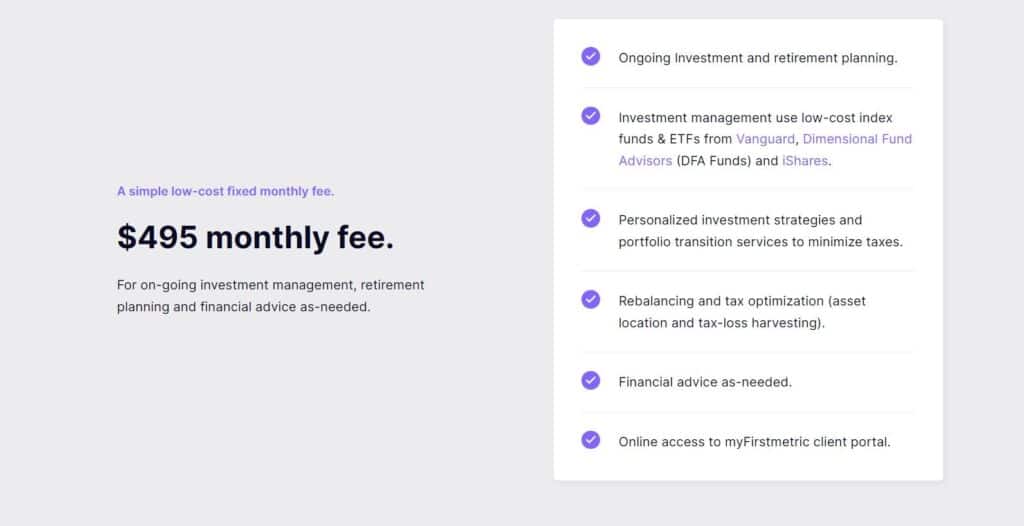

Check out the fees page for Scott Salaske, a flat fee advisor.

Very straightforward; almost like you are reading a menu in a restaurant. Alot of financial advisors are hesitant to put fees on their website. It’s manipulative and makes you look like you are hiding something.

According to Scott,

I try to minimize conflicts as much as possible starting with the way I charge fees to clients. Our fee is a fixed flat fee for on-going investment management and financial advice and guidance as needed.

Continuing with fees, I also post on our website in a clear, simple and transparent manner the fees that a client would pay to Firstmetric as their advisor. The vast majority of financial advisors do not. This is one of my biggest pet-peeves with “advisors” (term used loosely) in that they don’t want clients to know the fees that they pay or would pay otherwise they would simply make them public on their website.

-Scott Salaske, FIrstmetric

Bonus: the website fees actually match what it says in his company’s Form ADV and Form ADV Part 2!

#2 Listening for what the client really needs, regardless of what it means for you

Virtue is when you have the power to benefit at someone else’s expense and choose the reciprocal.

Chloe A. Moore, CFP® of Financial Staples is an incredible example of someone who is able to make rational choices for the client regardless of what it means for her.

Chloe is a Woman of Color, a group which is vastly underrepresented in wealth management, and she serves tech professionals in their 30s or 40s who often are women, People of Color, or LGBTQ+, many of whom are transitioning in their wealth journey from setting up the initial foundation to the next level.

People at this stage of wealth accumulation are particularly vulnerable, and unfortunately it is these types of folks who are preyed upon by product-pushing salespeople.

But Chloe takes a highly principled approach:

Many of my clients with equity compensation also have six figure student loan debt that causes a significant amount of stress. Instead of pushing them to sell their company stock and transfer the proceeds to me so I can build a diversified portfolio, we use a significant portion of the proceeds to accelerate debt payoff.

I’ve had a few clients receive large windfalls from an IPO. One client was very debt averse and wanted to pay off their mortgage. Knowing it would give them peace of mind, I encouraged them to do so.

-Chloe A. Moore, CFP

Although I could say more about this, I think her ethical actions speak for themselves. In many aspects, she takes the path less traveled, and she does it with objectivity, empathy, and grace. That’s what makes her a hero.

Chloe, I’m proud to stand behind you.

#3 Questioning if you can truly help the client in the first place

It’s all too common that advisors don’t have a clear target of who their services are best designed for. As a result, you see a division between the “A list” (the people they really want to serve) and the rest of the people paying them. But this financial advisor sees the person for who they are and how they behave, way moreso than their financial characteristics or how much money they have. I think it’s caused him to treat the client fairly in the example discussed below.

What do you think?

According to Krisna Patel, the client’s behavior is usually the determining factor when it comes to investment management. For that reason, he provides a DIY option that clearly specifies the differences in costs between DIY and his services. If the client has the wherewithal within a non-complex situation, he will often recommend they go the DIY route.

If he runs across a client with multiple accounts, he won’t necessarily recommend that all accounts be managed by his firm. He will talk with the client to determine the accounts which will benefit most from his services, because they will receive the same services regardless of the number of accounts he is managing.

Here’s an example.

The spouse of a client of mine recently asked me to provide a proposal for managing his SEP IRA, which he held directly at JPMorgan. I had been working with the couple for roughly three years and determined in our first few meetings that his SEP was in a lower cost allocation fund based on his risk tolerance. I had known him for years prior to our engagement and determined that he didn’t exhibit behavioral biases that might derail his long-term performance. Therefore, my initial recommendation was for him to keep the assets at JPMorgan rather than transfer. Over the years he had seen the value-add we provided for the household and was curious on the cost differences between keeping his funds at JPMorgan vs. transferring.

After getting the expenses together on his current SEP IRA, I sent a proposal explaining that his fee would go up roughly .2%/year (all in) by transferring the funds. Additionally, I explained that since his wife was a client of mine, he was already receiving the benefits of our firm without having his SEP with us, which entailed the meetings, financial planning services, and recommendations. By moving the funds with us he would simply be incurring a higher expense overall, since there was no additional benefit on the planning side above and beyond what he was already receiving.

I think this also speaks to the question above, in that we only want to engage and manage assets in which I believe we can provide value. This client didn’t exhibit behavioral biases in the years I had known him, he also seemed well versed in investment nomenclature and was in a good position to accomplish his goals. There was no reason to recommend he move the funds to a higher fee platform, especially since he was receiving the services via his wife’s engagement with our firm. A few months later he moved the funds over to our firm, mainly because he just wanted peace of mind and have everything with one contact.

-Krisna Patel, CFA

The highly ethical actions Krisna took were:

- Truthfully assessing if the client is better off doing it themselves

- Not just taking the business because he could get it

- Being willing to analyze the relationship at the account level to determine suitability for services

- Understanding the client’s emotional and behavioral makeup and seeing them as a person not just a portfolio

#4 Give the client the option for how they want to work with you

For advisors who are serving clients who have a diversity of needs, it can be hard to fit one price structure to them. AMC Wealth meets clients where they are, by providing a choice. Their fees are equitable and transparent.

The options are:

- AUM: From 1% (averages around 0.6%), this is best for a delegator who wants discretion

- Flat Financial Planning: $1,000 per year, this is recurring advice only, usually through a quarterly review

- Hourly Financial Planning: $200 per hour, this is one time/ad-hoc advice only

To quote Adam Cross, the founder:

Towards the end of all introductory meetings, we ask the prospect “how” they want to engage with us. Our first question is: “Do you prefer to work with us on a one time basis or do you prefer ongoing support?”

If the client tells us one time, we explain our hourly advice-only service. If the client prefers ongoing support, we will then ask them “Do you have a desire or need to have your account managed by us?” If no, we explain our flat advice-only option. If yes, we explain our % of AUM option.

If the client is unsure, we explain all 3, including the pros and cons of each, and help them choose.

-Adam Cross

What I like about this approach is that it puts the client in control of the relationship. Adam’s firm isn’t boxing anybody into one particular way of being serviced; this is ideal for DIY clients or people who want just a portfolio review. This is ethical because it puts the clients’ needs as the driver of the relationship instead of the advisor’s quota or their profitability. It avoids the need for the advisor to try to “sell” the client on one way of working with them which may not be a good fit at that point in time.

It also allows clients to be serviced in various capacities as their needs change. Maybe a client who is a resident radiologist with $300k of debt just wants a basic financial plan, but ten years later she may be married with a need for life insurance, a college planning strategy, and someone to manage her $1,000,000 portfolio. This kind of a set up could potentially create a very nice, fair experience for the client.

I love it when financial advisors treat small clients with decency!

#5 Hold your ego back during the decision process

I was so impressed with Jane Mepham of Elgon Financial Advisors who encourages prospects to go talk to the other advisors before they chose to hire her.

I repeat: she tells the prospect to interview other financial advisors while they are in the decision making moment.

That’s courage.

What an example of how to hold your ego back for the benefit of the child. This is the essence of objectivity, a trait so rare in our industry.

I want them to find an advisor they like and trust and I know I may or may not be that advisor. By the time they choose to work with me, they are 100% sure ( and will trust my recommendations), I’m the advisor for them, and it creates for a more trustworthy relationship.

-Jane Mepham

You see, alot of time people are so eager to close the deal that they skip right to the facts, questionnaires, and portfolio analysis without making sure the client is emotionally committed. By openly acknowledging that you aren’t the only one in the game, you make them feel you can relate to them more. Because you are. It’s unselfish and shows empathy, a great way to start the relationship.

#6 Just plain taking the high road

It’s one thing to say you “treat clients like family” – many financial advisors say that. It’s another thing to put your money where you mouth is, and mean it! At Envision Wealth Planning, James Brewer’s actions have shown himself to be true to his words.

One of our clients lost her job and was out of work for over a year. We continued to offer our financial planning services to them without compensation. When they got back on their feet, we allowed them to make up for these last payments on a schedule that was comfortable with their new cash flow. We all go through tough times. We don’t want to stop helping them just because they’re going through a rough patch.

-James Brewer

This vignette is an incredible example of:

- Empathy

- Human decency

- Meeting the client where they are

- Putting their needs before your own

- Having faith in the relationship

- Shining through in the moment of truth

- Acting out of your heart more than your mind

- Giving the client the benefit of the doubt

The tough times in life are when clients need their advisor the most. By refusing to allow his business needs to come before the client’s, James (in my view) acted, not just spoke but acted, as an advocate and likely made an unbelievable difference in this person’s life.

There’s something very, very true about that.

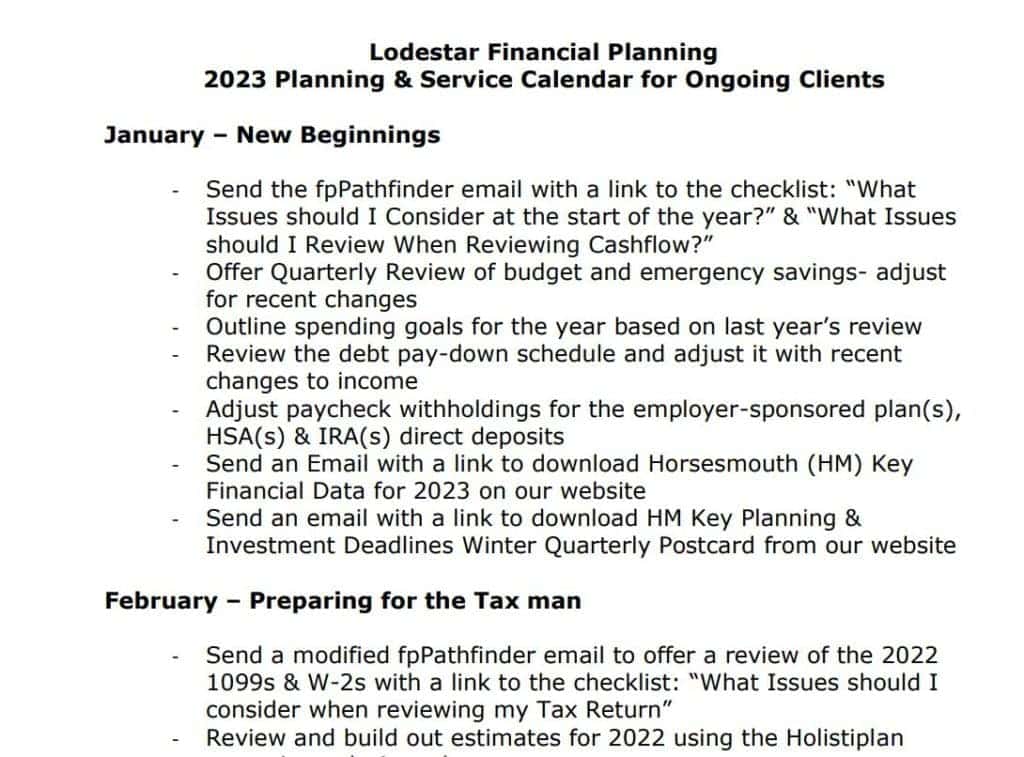

#7 Being transparent with clients about what the service ACTUALLY is

Skip Fleming of Lodestar Financial Planning does a fabulous job of making it abundantly clear to his clients about what the service entails. This is critical in the field of financial planning. Often financial plans are given away for free by insurance agents as a way to justify the client buying a whole life policy.

Financial planning, investment management, and any other services should be clearly described on your website and in all communication materials. It may seem like common sense but you’d be surprised at how much opacity exists and it makes it harder for the planner to justify the fees they are charging. Make it clear and leave nothing to assumption; you can never overclarify something.

Here’s an example of an advice-only financial planner who does a great job destroying the ambiguity, confusion, and lack of clarity that so often persists in the industry.

#8 Know who your client really is

When a financial advisor services a high net worth individual or family, it’s clear who the client is. But when advisors serve 401(k) plans, it can sometimes get lost.

In the employee retirement plan space, if you are a fiduciary, the client is the participants – even if you never meet or talk with a single one. Financial advisors miss this all the time. If they are working in the 401(k) space, their client isn’t the company, it’s not the CEO or someone in HR or some other group that hires them. It’s the participants. If you get that right, and eliminate the conflicts of interest, the rest is easy.

–Heath Miller, Access Retirement Solutions

Sara’s upshot on ethical financial advisor practices

I periodically blog about financial products and services so that consumers can avoid being taken advantage of by the financial services industry.

Please subscribe to my newsletter (free newsletter) to receive updates that raise awareness of consumer financial issues, so you can avoid being taken advantage of by shenanigans.

If you feel that you are a financial advisor with good ethical practices, send me a message and I’ll consider adding you to the list.

And btw, what’d ya think of my blog on ethical financial advisors? Was this helpful? If yes…

Join the Transparency Advisor Movement.

The Transparent Advisor Movement’s mission is to promote ideals of clarity, modesty, integrity, dignity, and client advocacy in all aspects of financial advice, with a special focus on Advice Only, Flat Fee, and Hourly service models. There is a special emphasis on clear disclosure of services and their related fees.

The Transparency Movement is the future of the industry – we welcome anyone who believes in our values to join us.

Join our next Transparent Advisor virtual meetup.

These meetups are free and the goal is to learn from each other about how to grow and manage a transparent practice for the benefit of clients.

Even if you can not make the meetup, or even attend in its entirety, please register for the replay and to be notified of the next one.

Or if you are looking to market yourself better…

Learn what to say to prospects on social media messenger apps without sounding like a washing machine salesperson. This e-book contains 47 financial advisor LinkedIn messages, sequences, and scripts, and they are all two sentences or less.

You could also consider my financial advisor social media membership which teaches financial advisors how to get new clients and leads from LinkedIn.

Thanks for reading. I hope you’ll at least join my weekly newsletter about financial advisor lead generation.

I also have a newsletter for advice only, hourly, and flat fee advisors.

I hope you got the chance to check out my marketing and practice management tips for advice only, hourly, and flat fee advisors.

See you in the next one!

-Sara G

Disclosures

Grillo Investment Management, LLC does not guarantee any specific level of performance, the success of any strategy that Grillo Investment Management, LLC may use or mention in any of its content, or the success of any program it may mention in any of its content.

Grillo Investment Management, LLC will strive to maintain current information however it may become out of date. Grillo Investment Management, LLC is under no obligation to advise users of subsequent changes to statements or information contained herein. This information is general in nature; for specific advice applicable to your current situation please contact a consultant or advisor. There is nothing that guarantees that the information presented in this article or on this website is accurate.

Also, nothing in this podcast or blog can be interpreted as legal or compliance advice. For advise on such matters, contact a legal or compliance advisor.