This blog is not for the faint of heart. I am writing it because I’m sick of the BS narratives perpetrated by the financial media, a prime example being the Barron’s Top Advisor List. There are other nonsense financial advisor rankings such as Forbes and CNBC that I rip apart here too. I’m keeping a running tally of these BS advisor ranking lists and please let me know if there are any I am missing, I’ll put them on my hit list.

For those of you who are new to my blog/podcast, my name is Sara. I am a CFA® charterholder and financial advisor marketing consultant. I have a newsletter in which I talk about financial advisor lead generation topics which is best described as “fun and irreverent.” So please subscribe!

But before I start the ripping…

First, let’s why the whole concept of a financial advisor rankings is bogus in the first place – or at least one composed in the fashion as the Barron’s list. There is no absolute value that can be quantified by a few simple metrics and a simple questionnaire. Different advisors are great for different clients. There was an indexing system envisioned by Brent Weiss of Facet Wealth, described in this article by Bob Veres. Any system that attempts to quantify and rank the value of an advisor should be multi-faceted and the basis for its output should be clear and transparent.

Let’s also discuss what the purpose of financial advisor rankings should be. Theoretically it should be to identify the most effective financial advisors so that the public can be better served by having more visibility, and hence access, to them, as opposed to the supposedly less effective ones who aren’t on such lists.

Notice I said the word “theoretically.” Many consumers are still hesitant to trust any financial advisor that they do not know personally or who has not been “vouched for” by someone they trust. Financial advisor rankings, if they were better constructed, could potentially serve this purpose but the reality is these lists are not well-vetted, highly biased, and intended to placate the more popular and influential players within the industry rather than serve the consumer.

The Barrons’ Top Advisor List… is just terrible

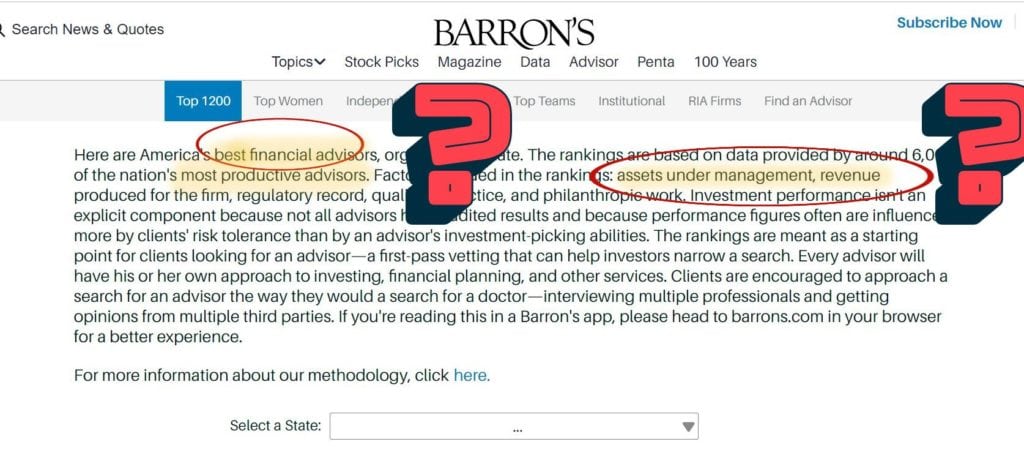

Here is the Barron’s 2022 Top Advisor Rankings by State.

Here is the methodology used.

I’m about to get it into it, but wow, just wow.

In case you couldn’t read the words above, it says:

“Here are America’s best financial advisors, organized by state. The rankings are based on data provided by around 6,000 of the nation’s most productive advisors. Factors included in the rankings: assets under management, revenue produced for the firm, regulatory record, quality of practice, and philanthropic work. Investment performance isn’t an explicit component because not all advisors have audited results and because performance figures often are influenced more by clients’ risk tolerance than by an advisor’s investment-picking abilities. The rankings are meant as a starting point for clients looking for an advisor—a first-pass vetting that can help investors narrow a search. Every advisor will have his or her own approach to investing, financial planning, and other services. Clients are encouraged to approach a search for an advisor the way they would a search for a doctor—interviewing multiple professionals and getting opinions from multiple third parties. If you’re reading this in a Barron’s app, please head to barrons.com in your browser for a better experience.”

Just reading this makes me SICK – want to rip it down off the internet, people!

#1

The opening line “here are America’s best financial advisors” – are you KIDDING me????

So first they say “these are the best advisors” and then in the next line they quickly redact, identifying them as “the nation’s most productive advisors.”

First of all, that’s confusing. Effectiveness is one thing, and production is another.

Second of all, for those of you who aren’t familiar with the industry, “production” is an industry term from the old guard, representing the amount of products a stock broker sold. To see this term blurred with the top advisor definition, it makes me mad because it implies that advisors who are selected on the basis of production – and this gives me the sense that this ranking had a lot to do with precisely that – are the best financial advisors. This presumption is WRONG. Selling a product does not equal financial advice.

Consumers shouldn’t be misled in any way and the way this shoddy explanation – if I could even call it that – is written, it’s almost as if they are trying to obfuscate something.

Maybe it is just poorly written and an honest oversight. But to me it’s as if they are explaining in order to check the box but not really the total explanation with complete clarity, which consumers deserve.

The consumer always deserves the complete truth – not sure we’re getting it 100% here. It’s the typical financial services move of providing enough information to satisfy the minimum standard of transparency, but never going to the full extent that would enable the person to know what is really going on.

#2

There not that much clarity provided as to how this “top advisor list” was composed. They say they based the rankings on:

- Assets under management (AUM)

- Revenue produced for the firm

- Regulatory record

- Quality of practice

- Philanthropic work

I’ll get into why these metrics are flawed in a minute, but first I want to make the point that without knowing the extent to which each of these factors were weighted, there’s no way we can know what the output of the selection methodology represents. If the AUM factor were 50% of the advisor’s score, that is heavily biased towards the advisors with larger practices (who aren’t necessarily the most effective, they might just be the best salespeople, who knows).

On top of that, these are crappy metrics if you are trying to compile a list of who the top advisors are.

AUM – a financial advisor may have a large practice by AUM if they bought another practice (and you wouldn’t know that unless you saw their balance sheet and the huge debt balance looming there). Or they could perhaps just have a lot of clients that they pay zero attention to, which I have personally seen firsthand and it’s painful to watch.

Revenue produced for the firm – This is likely also related to the size of the advisor’s business. Financial advisors who charge a percentage fee based on AUM will bring in more revenue. Or, advisors who hustle and sell aggressively, push products to meet sales quotas, all the while neglecting their clients that they already “sold” – those are the people who may rank high by this metric. Revenue is not an indicator of the effectiveness of the advisor any more than the number or size of clients they have is.

Regulatory record – People who break the law shouldn’t be allowed in the industry. It’s ridiculous. I’ve seen convicted criminals, people who stole tens of thousands of dollars, still be allowed to work in the field handling people’s money in some capacity.

What regulatory research specifically did they do? Did they look at everyone’s ADV? As of what date, if they looked at the ADV? What type of “regulatory history” was disqualifying, specifically? A speeding ticket? A felony?

Although it’s good to have some factor here that filters out the people with regulatory records, it’s not that useful in terms of helping to evaluate one candidate versus the next. So the advisor who ran a $5MM Ponzi scheme scores worse by this factor than the one who ran a $1MM Ponzi Scheme? Guess what – both of them should have been excluded in the first place. It’s binary – no criminals should be included in the candidate pool. This should be an elimination factor that precludes people from being included on a financial advisor rankings list, not one used to rank one advisor relative to the other.

Quality of practice – YES finally one factor I agree with. But Barron’s – how did you measure that?

- Amount of hours dedicated to client?

- Client satisfaction survey?

- Response time to client?

- Number of employees per client?

- What about advisor/client ratio?

- What about fiduciary standard?

- What about fairness or transparency of fees?

- What about straightforwardness of communication?

- What about ethics?

- Impact on the client?

- Selection process for investments – avoiding high fee, embedded fee, products?

- Presence of conflict of interest, or lack thereof, within pricing structure?

- Quality of financial planning services rendered? Depth of financial plan?

Philanthropic work – Look, I’m a charitable person myself. But I don’t think that makes anyone a better, more effective financial advisor for their clients. It’s virtue signaling. This is a nonsense factor that has zero relevance to a financial advisor rankings list.

Overall, in my opinion these are not very useful factors. They measure superficial traits and depending upon how they are weighted could potentially allow advisors who excel in sales and marketing, many of whom work for the large wirehouses who hold their reps to a quota – to rank better than those who deliver quality advice to clients.

#3

There is not that much clarity as to evaluation process they followed.

- Did Barron’s ask an advisor fill out a form (that the advisor’s 20 year old intern probably completes for them) and then you apply a formula based on assets, revenues, and quality of practice (???).

- How many advisors applied?

- How did these advisors get invited to apply?

- Was the universe big enough or was there selection bias? How do they know they got a true sample in order to call the selected few the best?

- How did they get the list of advisors to send the questionnaire to?

- They state they did

They wind up picking 1,200 advisors through this process. Are there even 1,200 top advisors out there? I mean, really.

#4

“The rankings are meant as a starting point for clients looking for an advisor.”

And then at the end they encourage readers to use it as a starting point to find a financial advisor. Are you kidding me.

No words, people.

My take on the “Forbes America’s Top Wealth Advisors List” – is this a joke?

Forbes also publishes financial advisor rankins. Similar story here as to Barron’s, although not as egregious.

One thing I do like about the Forbes top advisor list is that the process seems a bit more in depth. As discussed on the methodology page, SHOOK Research (an independent firm) conducts research and they do some actual interviews, over Zoom, phone, or in person. But that’s where, for me, the merits of these financial advisor rankings end.

I have several issues with the methodology, namely:

- The advisor must have an “acceptable compliance record.” Huh? When are we going to stop making excuses and let advisors wiggle out of their wrongdoings? There are plenty of financial advisors with a long tenure in the business and spotless compliance records. I don’t know why we have to mention anyone whose ability to comply with regulation has ever been called into question.

- They list out the metrics, but don’t really discuss how they are weighted.

- The use discussions with management and peers as a factor. Why? Don’t you realize that is like asking the barber for a haircut? You don’t realize these are some of the best trained salespeople on planet Earth? If you want to know what they are really like, why don’t you ask the advisor to provide the name of a past client who doesn’t do business with them anymore – and then see how the story changes.

- Not alot of clarity on the “client-related data” factor, which is the only one of the three listed there that I find to be meaningful., and there’s no in-depth indication of what the weighting of this factor is, or what data is actually assessed. The others – AUM and revenue/production, as with Barron’s, can be more of an indicator of sales skill.

- Community involvement is a qualitative factor. What exactly is that in terms of how it’s being defined for this purpose, and how does that make an advisor more effective?

- On the page where the advisors are listed out, it says, “Presented by Charles Schwab.” Huh? Why don’t you tell us how Schwab is involved, please?

If you look at who Forbes has in their financial advisor rankings, it’s pretty clear there is a large representation of wirehouse financial advisors. Those are typically advisors who charge commissions, either as their sole form of compensation or in combination with AUM fees. These are pretty conflicted business models, and these wirehouses operate in a pretty quota-driven environment. That can tell you something about this magical algorithm they describe in the methodology section.

In my view, the Forbes top advisor list is another terrible example of misleading the public for the purposes of placating the ego and agenda of the big dogs in the industry. And in the meantime there are thousands of advisors out there who go completely unnoticed to the public providing stellar service that puts the consumer first.

Pathetic.

My take on the CNBC Financial Advisor 100 – “meaningless” is an understatement

The CNBC financial advisor rankings list was so badly compiled, it made the task of ripping it apart easy.

The CNBC top advisor list uses a third party to gather data from the advisor universe – so they get a point for that – but unfortunately that’s where the merits of the selection methodology end, in my opinion.

- Data analyzed includes advisor’s compliance record, but it’s unclear as to what types of infractions were allowed/disallowed. In my view, as I’ve stated above, any infraction should grounds for being ruled out, but it’s murky here as to the extent to which that matters in CNBC’s eyes.

- Description of each evaluation factor was very cursory and vague to the point of being nearly useless to have even bothered listing them out. Not helpful to the consumer reading this wondering if the advisors named are truly worthy or if the methodology was shoddy.

- Number of years in the business included as a factor. Not sure why this matters that much. I’ve seen advisors two years in the business do a bang up job.

- Number of employees included as a factor, and number of employees vs. number of advisors. WHO cares? I’d be more interested in the number of employees or advisors vs. number of clients.

- AUM, discretionary AUM, and number of accounts were factors. As with Barron’s and Forbes, this again could be more of a signal of the company’s interest in putting business development as a priority.

- There was not one single indicator on this list focused on assessing the advisor’s quality of service, impact on clients, retention, amount of time dedicated to clients, etc. Isn’t that what really matters? Shouldn’t that be what these financial advisor rankings should be based on, rather than who is the biggest on paper?

- Based on the methodology description, it seemed there was not even a questionnaire sent to advisors to fill out or any kind of interview, but rather just an analysis done on data from a third party provider. If this was just based upon a reading of the raw numbers with no verification of them from the advisor him or herself, that is a possible weakness.

According to the publication itself, “The CNBC FA 100 recognizes those advisory firms that best help clients navigate their financial lives.” If you look at the criteria this list is based on, by CNBC’s own disclosure, then this is a ridiculous statement and one that does not confer with reality.

Maybe there was more intelligence engrained in this process behind the scenes, somehow, but it doesn’t seem like it from what I’m reading here. I really wish CNBC could have put more thought into these evaluation factors because overall the criteria used to determine who should be on the list, to me, are pretty meaningless. This is the type of thoughtless journalism that damages consumers, in my view.

InvestmentNews 40 under 40

Here’s my unfavorable view of the InvestmentNews 40 under 40.

#1 Questionable selection process

There was no mention of any sort of quantitative ranking system, just review by an editorial committee and a list of factors. How can there be any objective standard then? Did they score the applicants or was it just whoever sounded the best and/or had the best recommendation wins? Their description of the selection process was a bit vague and to me, calls into question its soundness.

#2 Weak factors

The criteria are ridiculous, as stated: accomplishments, contribution, leadership, promise. And what is the “promise” category anyways? Since when does someone get an award based on potential; it’s like predicting the weather to try to gauge one person’s potential vs. another. Are you kidding me?

And this list of factors stinks.

What about ethics, client focus, transparency of fees and business practices, professional licenses and credentials, absence of conflicts of interest, objectivity, promotion of fairness to client, amount of attention paid to the end clients, responsiveness to client needs.

These don’t matter?

So it’s okay to identify leaders based on what they appear to be contributing to the public, without a consideration for how their work actually impacts the end client?

They say that they need to know who the nominator is, and you can’t do this anonymously. Why? Sounds like a move to perpetuate the “cool kids club.” So that if someone with influence, whom they like, nominates you, you’re already “vouched for” so to speak? Why should it matter who the nominator is? The fact they have to know who nominated you indicates how highly biased this list is – and not objective.

And there are other things that just plain don’t make sense.

- There are more than 1,000 nominees reviewed by the editorial team. How many people are on this team, and how do they have time to review hundreds of applications in depth? Huh?

- No note given to whether or not they verify any information about the people nominated. Were ADVs checked? That in itself, for 1000 applicants, is a full time job.

- No disclaimer included saying that this is not an endorsement and consumers should do their own research. Without such a disclaimer, these lists can be very misleading.

- The concept of excluding people over a certain age is ageist. The Older Workers Benefit Protection Act, Age Discrimination in Employment Act, and many state laws protect older workers, identified as those above 40. This is precisely whom InvestmentNews is looking to exclude!

Investopedia Top 100 Financial Advisors is a 7th grade popularity contest

When I look at the bullcrap financial rankings put forth in the Investopedia Top 100, I really feel like I am transported back to my 7th grade gym class where the cool kids got picked first for dodgeball.

Investopedia states, “With more than 100,000 independent financial advisors in the U.S., the Investopedia 100 spotlights the country’s most engaged, influential, and educational advisors.”

Really? So you checked out all 100,000 advisors? Or are you just mentioning this number to make it seem like you did, because otherwise what is the point of calling attention to this amount?

Moreover, there’s zero explanation for the 2021 list as to how these advisors were selected. It is totally irresponsible and misleading to the consumer to put forth a list of people you are calling “top advisors” and then not even justify why these financial advisors were “ranked” this way. Where there is no explanation, no credibility is awarded.

However, if you look to a year before, the 2020 Investopedia Top 100 list page states:

Investopedia’s proprietary methodology focuses on awarding financial advisors who have demonstrated a top-of-the-industry ability to reach the largest and most diverse financial and investing audience. That reach is measured by the impact and quality of the advisor’s published work, public appearances, online following, and commitment to financial literacy across diverse communities. The 2020 Investopedia 100 also heavily weighed peer-to-peer nominations, highlighting the most influential advisors who were recommended by their peers.

Source: https://www.investopedia.com/top-100-financial-advisors-5081707

What a joke.

I mean, they come out and say it: “the 2020 Investopedia 100 also heavily weighed peer-to-peer nominations”.

Coupled with the fact that they measure the advisor’s influence by their online following (Twitter, in many cases), to me this list represents nothing more than the social media “cool kids” club.

So let me get this straight.

To get on this list, someone could conceivably just hang out on social media platforms all day, virtue signal, pander, post pictures of their kids, and/or socially stair climb enough to where all the people following the FinTwit twitter threads like him or her well enough to recommend them for this list. Many of them do this, by the way.

Did I get that right?

In my view, this is not a sound way to measure an advisor’s influence. There’s no elaboration as to how they measured the quality, commitment, or impact. Is quality, for example, measured by how many comments the advisor’s posts get? Shares? Likes? The eventual actions taken by the readers of these works?

From what I’ve seen, many financial advisors’ followings are heavily populated by other financial professionals. Who in their audience are they really helping – the underserved? Or is it just other advisors? I’m not sure this was well thought out as no evidence is provided to make me think so. There’s no indication of if the measurement was based on vanity metrics or real life changing occurrences. For all these reasons, I don’t see the selection methodology as very credibility-garnering.

Is a financial advisor the most influential just because they tweet all day, as many on twitter’s Fintwit do? Why aren’t they diligently focusing on their clients, or on the public they are so committed to helping through their published works? Should we be awarding advisors for being talking heads/media personalities? If so, where are Suze Orman and Dave Ramsey – why aren’t they on this list?

Moreover, the titling of this list is wrong IMO. It’s not really the top 100 financial advisors, because that would imply there was some measure of effectiveness. By its own definition, this list identifies the most influential financial advisors (supposedly). The list therefore should be called, “Top 100 most influential financial advisors” instead instead of this aggrandizing, bogus, clickbait title.

For all of the above reasons I see this (supposed) financial advisor ranking list as nothing more than the annual industry popularity contest. It doesn’t serve the public to put forth lists like this.

Financial advisor rankings suck!!!!

Here’s what I’m doing to overshadow these crap financial advisor rankings and get them replaced by guidance to consumers that actually supports positive outcomes. I’m sick of consumers getting misled by crap financial advisor rankings like this, and I want to see more clarity about who the real advocates are who will deliver an experience to them that is less conflicted and more focused on truly helping the client with their finances instead of just lining the advisor’s pocket.

I made a few of my own lists. But remember, none of these are recommendations or endorsements of any advisor mentioned here – you must do your own independent research on any financial advisor you are thinking about doing business with.

Ethical actions that financial advisors take

If you or anyone you know should be on these lists, let me know. I really want consumers to see a new image of the kind of financial advisor they should seek to work with, one who is:

- Honest

- Straightforward

- Clear in communication

- Modest

- Client-focused

- Genuine

- Modest

- Following a model that maximizes transparency and minimizes conflict of interest

- An advocate

- Services rather than sale or product focused

- Interested in making the clients free rather than locked up

Join the Transparency Advisor Movement.

The Transparent Advisor Movement’s mission is to promote ideals of clarity, modesty, integrity, dignity, and client advocacy in all aspects of financial advice, with a special focus on Advice Only, Flat Fee, and Hourly service models. There is a special emphasis on clear disclosure of services and their related fees.

The Transparency Movement is the future of the industry – we welcome anyone who believes in our values to join us.

Join our next Transparent Advisor virtual meetup.

These meetups are free and the goal is to learn from each other about how to grow and manage a transparent practice for the benefit of clients.

Even if you can not make the meetup, or even attend in its entirety, please register for the replay and to be notified of the next one.

And now I’m going to bed!

Thanks for reading my rip of the top advisor lists. I’ve enjoyed writing it, but now I have to go to bed.

I periodically blog about financial products and services so that consumers can avoid being taken advantage of by the financial services industry.

Please subscribe to my newsletter (free newsletter) to receive updates that raise awareness of consumer financial issues, so you can avoid being taken advantage of by shenanigans.

If you are a financial advisor looking to market yourself with more fairness, logic, and transparency:

- I am an outsourced CMO for companies who need regular, full service marketing – blogging, social media posts, newsletters, etc.

- I am an hourly consultant for those who just need one-time or recurring guidance

- People hire me as a ghostwriter to write content for a project fee

- I have a social media training program

- I have a book about what to say on LinkedIn messenger

Just letting ya know, in case you need me at some point.

-Sara G

Thanks for reading. If none of this appeals, I hope you’ll at least join my weekly newsletter . I write about financial advisor lead generation, practice management, etc. and in the future I am going to write more on these BS top advisor lists.

See you in the next one!

-Sara G

Sources

Barron’s 2022 Top Advisor Rankings by State. Retrieved on June 2nd, 2022 from https://www.barrons.com/advisor/report/top-financial-advisors/1000

Barron’s Top Advisors Methodology. Retrieved on June 2nd, 2022 from https://www.barrons.com/articles/barrons-methodology-for-ranking-financial-advisors-51615843316

Forbes America’s Top Wealth Advisors. Retrieved on June 3rd, 2022 from https://www.forbes.com/top-wealth-advisors/#3ace16241a14

Methodology: America’s Top Wealth Advisors 2021. Retrieved on June 3rd, 2022 from https://www.forbes.com/sites/rjshook/2021/08/24/methodology-americas-top-wealth-advisors-2021/?sh=1d6e4a2f649c

CNBC. (6 October, 2021). Financial Advisor 100. Retrieved on June 4th, 2022 from https://www.cnbc.com/2021/10/06/fa-100-cnbc-ranks-the-top-rated-financial-advisory-firms-of-2021.html

Pavia, Jim. CNBC. Here’s how we determine the FA 100 ranking for 2021. Retrieved on June 4th, 2022. https://www.cnbc.com/2021/10/06/heres-how-we-determine-the-fa-100-ranking-for-2021.html

InvestmentsNews. 40 Under 40. Frequently Asked Questions. https://investmentnews40under40.secure-platform.com/a

InvestmentsNews. 40 Under 40. https://40under40inadvice.com/

Investopedia. Investopedia Top 100 Financial Advisors of 2021

Investopedia. Investopedia Top 100 Financial Advisors of 2020

Disclosures

Grillo Investment Management, LLC does not guarantee any specific level of performance, the success of any strategy that Grillo Investment Management, LLC may use or mention in any of its content, or the success of any program it may mention in any of its content. Grillo Investment Management, LLC will strive to maintain current information however it may become out of date. Grillo Investment Management, LLC is under no obligation to advise users of subsequent changes to statements or information contained herein. This information is general in nature; for specific advice applicable to your current situation please contact a consultant or advisor. I want to be clear that nothing in this podcast or blog can be interpreted as an investment recommendation of any type, or an endorsement of any particular person or their services. The opinions expressed herein do not necessarily represent the views of Sara Grillo or Grillo Investment Management, LLC. Also, nothing in this podcast or blog can be interpreted as legal or compliance advice. For advise on such matters, contact a legal or compliance advisor. Any similarities to persons deceased or alive are entirely coincidental.